However, while the changes may be straightforward for some organisations, for others they introduce an important governance decision — particularly around whether to move from Charities SORP accruals accounts to receipts and payments accounting.

For some charities, this will be simple:

-

If you are a charitable company, your reporting framework does not change.

-

If your structure and funding are straightforward, the new flexibility may be easy to assess.

For others — especially those with material gifts in kind, timing differences, investments, property, or sensitive reserves — the decision requires more careful evaluation.

In this article, we cover:

-

What the new threshold changes are and when they take effect

-

How the timing interacts with SORP 2026

-

A worked example of how the changes apply in practice

-

Who can and cannot move to receipts and payments

-

What receipts and payments does well — and what it does not

-

A structured decision framework to help trustees evaluate what reporting basis is right for their charity

The new thresholds offer flexibility — but flexibility brings responsibility. The right decision depends on your charity’s individual circumstances.

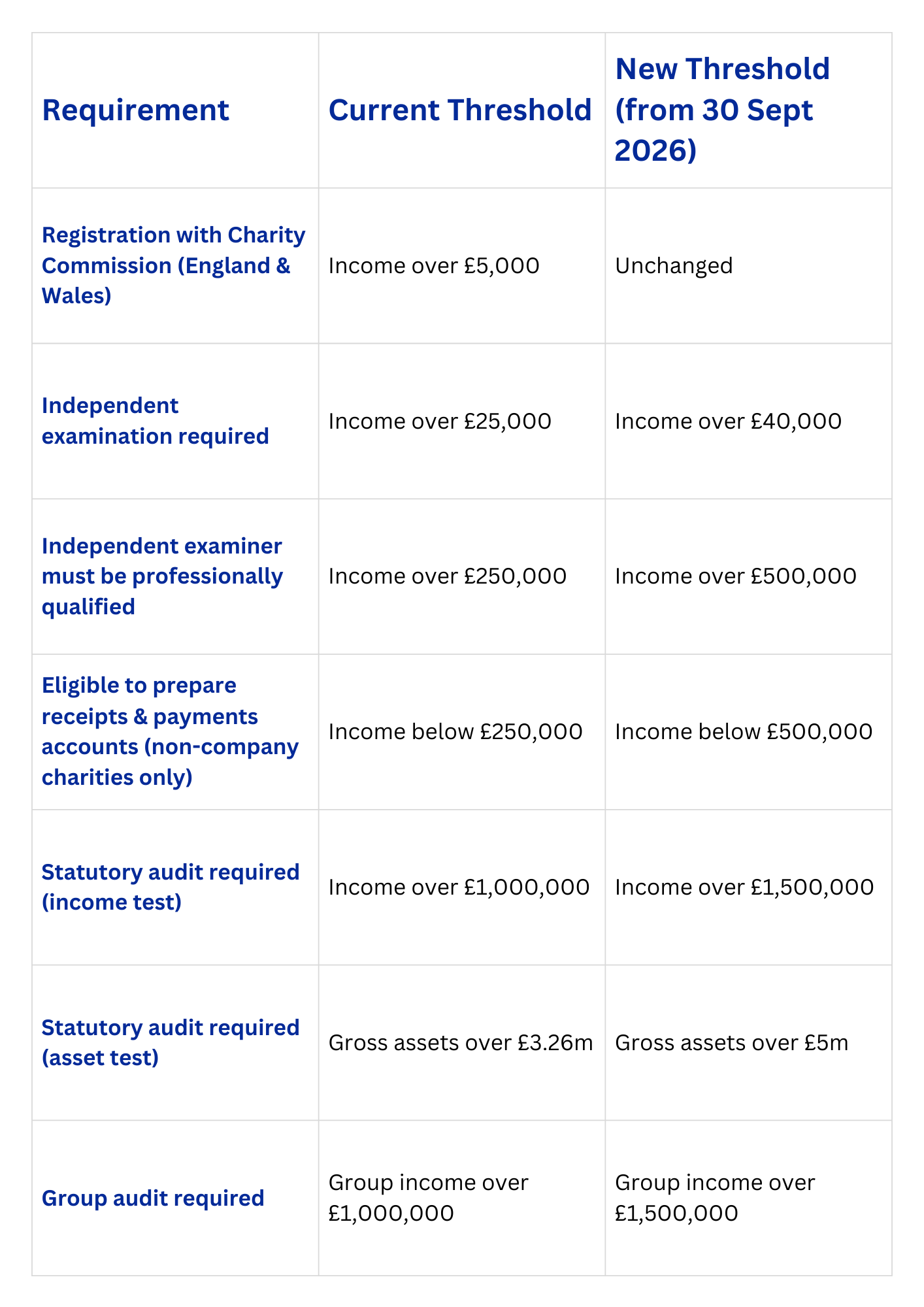

What’s Changing — and Should You Switch to Receipts & Payments?

What’s Changing?

Important Timing Point: SORP 2026 Starts First

Worked Example: 31 March 2026 Year End

Let’s take a charity with:

- Year end: 31 March

- Income: £450,000

Year ended 31 March 2026

- This period began 1 April 2025.

- It is before the new threshold change date (30 September 2026).

- The charity must follow the existing thresholds.

- Because income exceeds £250,000, it must prepare accruals accounts under the Charities SORP.

Year ended 31 March 2027

- This period ends after 30 September 2026.

- Income is still £450,000.

- Under the new thresholds, the charity would now be eligible to prepare receipts and payments accounts instead of SORP accruals accounts

But — and this is crucial — it now has a choice.

Eligibility does not automatically mean it is the right move.

A Very Important Reminder: Charitable Companies Cannot Switch

If your charity is:

- A limited company, and

- Registered at Companies House

You must continue preparing accruals accounts under the Charities SORP, regardless of income level.

Company law requires this.

The receipts and payments option is only available to non-company charities that meet the income criteria.

Are Receipts & Payments Accounts Really Better?

If your charity’s income falls below the new £500,000 threshold, you may now be eligible to prepare receipts and payments accounts.

But eligibility does not automatically mean it is the right move.

Receipts and payments accounts are designed to be simpler. They focus purely on:

- Cash received during the year

- Cash paid during the year

- The cash balance at year end

For very small charities with straightforward activity, limited commitments, and minimal complexity, this approach can work well. It is easier to prepare, easier to understand, and may reduce professional costs.

However, trustees should pause before assuming that “simpler” automatically means “better”.

What Receipts & Payments Does Well

Receipts and payments accounts:

- Provide a clear picture of cash movement.

- Are relatively straightforward to prepare.

- Can be appropriate where transactions are simple and timing differences are minimal.

- May reduce the reporting burden for smaller charities with limited financial risk.

For charities that operate almost entirely on a cash basis — with no significant grants spanning year ends, no major assets, and no complex funding arrangements — they may be entirely suitable.

What Receipts & Payments Does Not Show

However, receipts and payments accounts do not:

- Show unpaid bills (creditors).

- Show income earned but not yet received (accrued income).

- Reflect grant income recognised over time.

- Present debtors and creditors clearly.

- Recognise significant commitments or provisions.

- Present a full balance sheet in the same structured way as SORP accruals accounts.

- Demonstrate a “true and fair view” in the same comprehensive sense as accruals accounting.

This means the reported result for a year can be materially different depending purely on when cash happens to move.

How Do We Make an Informed Decision?

If your charity’s income falls below £500,000, you may now have a choice.

But the right reporting basis is not about what is legally permitted — it is about what best reflects your charity’s financial reality and supports good governance.

Before deciding to move to receipts and payments, trustees and key management could work through the following structured questions.

Step 1: Complexity – How Simple Are We Really?

- Do we have multiple restricted or designated funds?

- Do we carry forward grant balances from one year to the next?

- Do we operate a trading subsidiary or prepare group accounts?

- Do we hold property or significant fixed assets?

If the structure is complex, accruals accounting may better reflect reality.

Step 2: Timing – Does Cash Reflect Performance?

-

Do we receive grants in advance for future activity?

-

Do we regularly accrue income at year end?

-

Do we have significant unpaid bills or year-end accruals?

-

Are legacy receipts recognised before cash is received?

-

Would removing accruals materially change how a year appears?

If timing differences are significant, receipts and payments may distort performance.

Step 3: Reserves – Is Our Position Sensitive?

-

Is our reserves level tight or closely monitored?

-

Would removing creditors or accrued income materially change our reported reserves?

-

Do funders rely on our reserves disclosure?

-

Could receipts and payments make us appear artificially stronger or weaker?

Where reserves are sensitive, accruals accounting usually provides a clearer picture.

Step 4: Investments & Non-Cash Activity

-

Do we hold material investment portfolios?

-

Are gains and losses significant year to year?

-

Do we receive substantial gifts in kind (e.g. food bank stock, donated goods, donated services)?

-

Do we receive significant donated assets?

If non-cash transactions are material, receipts and payments may understate the scale of activity.

Step 5: Long-Term Commitments

-

Do we have lease liabilities (particularly under SORP 2026)?

-

Do we have defined benefit pension liabilities?

-

Do we have long-term funding commitments or provisions?

Receipts and payments reduces visibility over long-term obligations.

Step 6: Governance & Perception

-

Do funders expect SORP accounts?

-

Would simpler accounts reduce clarity for trustees?

-

Would stakeholders view the change as reduced transparency?

-

Would it affect confidence in our stewardship?

Accounting is not just technical — it shapes how your charity is perceived.

Step 7: Future Planning

-

Are we planning growth, a major appeal, or a capital project?

-

Are we likely to exceed £500,000 again soon?

-

Would switching now only to revert later create disruption?

Switching accounting basis twice within a few years can add unnecessary complexity.

A Simple Decision Rule

Ask yourselves this:

Would moving to receipts and payments materially change how an informed reader understands our financial health?

If the honest answer is “yes”, then remaining on SORP accruals accounting may be the more responsible and transparent choice — even if you are legally allowed to simplify.

The Bottom Line

Falling below £500,000 gives you flexibility.

It does not remove your responsibility to present meaningful, transparent financial information.

For some very small charities with straightforward finances, receipts and payments will be entirely appropriate.

For others — particularly where there are:

-

Complex restricted funding

-

Significant timing differences

-

Material investments

-

Property or lease commitments

-

Sensitive reserves

— SORP accruals accounting may better support good governance and informed decision-making.

The decision should be deliberate, documented in trustee minutes, and taken with professional advice where appropriate.

Need Support Deciding?

Choosing the right reporting basis is not simply a compliance exercise — it’s about presenting a fair, meaningful picture of your charity’s financial health and ensuring trustees can make informed decisions with confidence.

Every charity’s circumstances are different, and what is appropriate for one organisation may not be right for another.

If you would like support in reviewing your structure, reserves position, funding arrangements or future plans before making a decision, do feel free to get in touch with the team at Wyatt & Co Chartered Accountants at office@wyattandco.net

. We would be very happy to help you evaluate what reporting framework is best suited to your charity.